Variable Annuities Surge in Popularity as Alternatives to Restricted Investment Products

Sales of variable annuities at major South Korean banks have skyrocketed nearly tenfold in the past three years. This surge is attributed to a confluence of factors: a robust stock market, the appeal of tax-advantaged investment options, and banks’ strategic efforts to bolster non-interest income. However, experts caution that the potential for disputes, mirroring those seen with Derivative Linked Funds (DLF) and Equity Linked Securities (ELS), necessitates enhanced risk disclosures and consumer protection measures.

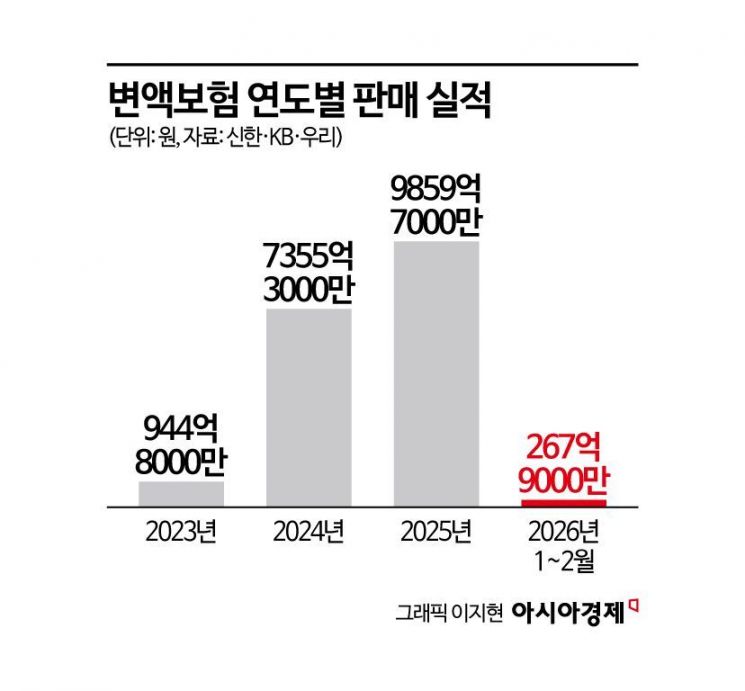

From ELS Restrictions to Variable Annuity Boom

The dramatic increase in variable annuity sales began in 2024, coinciding with restrictions placed on the sale of ELS products following significant investor losses. As ELS sales dwindled, banks actively promoted variable annuities as an alternative, seeking to offset the decline in fee income. A bank representative noted the need to actively promote alternative products after ELS sales became difficult.

The favorable market conditions of 2024, with the KOSPI index experiencing a remarkable 76% annual increase, further fueled demand. Investors, both high-net-worth individuals seeking tax benefits and individual investors looking to diversify their portfolios, were drawn to the potential for higher returns through variable annuities.

Changing Fee Structures and Future Sales

Looking ahead, banks anticipate a moderation in the growth of variable annuity sales. A key factor is a recent regulatory change by financial authorities requiring banks to recognize sales commissions over a period of up to 10 years, rather than immediately. This shift reduces the short-term financial incentive for banks to aggressively market these products. Increased market volatility, triggered by geopolitical events, is also dampening investor enthusiasm.

Potential Risks and the Need for Enhanced Disclosure

Despite their growing popularity, variable annuities carry inherent risks. As investment-linked insurance products, their value is directly tied to the performance of underlying assets. A decline in the stock market can lead to reduced insurance benefits or lower surrender values. This raises concerns about potential mis-selling and inadequate risk disclosure.

Professor Seo Ji-yong of Sangmyung University emphasizes the importance of clear communication, stating, “Variable annuities are often confused with deposit products at bank branches, and incomplete sales occur due to insufficient explanation.” He warns that, similar to the DLF and ELS incidents, disputes could escalate during periods of market turbulence.

Professor Choi Jae-won of Seoul National University highlights the unique trust consumers place in banks, stating, “Consumers tend to believe that banks offer safer financial products than other institutions.” He argues that banks have a heightened responsibility to thoroughly disclose potential losses and volatility, mitigating the risk of investor harm.

Frequently Asked Questions

- What is a variable annuity? A variable annuity is an insurance contract that allows investors to allocate premiums to various investment options, such as stocks and bonds. The value of the annuity fluctuates based on the performance of these underlying investments.

- What are the risks associated with variable annuities? The primary risk is market risk – the potential for loss due to declines in the value of the underlying investments.

- How are variable annuities different from ELS? While both are investment products, variable annuities are insurance products with tax advantages, while ELS are structured securities linked to the performance of specific assets.

- What is the role of banks in selling variable annuities? Banks act as distributors of variable annuities, offering them to their customers as part of their broader financial product offerings.

Pro Tip: Before investing in a variable annuity, carefully review the product prospectus and understand the associated fees, risks, and potential returns.

Explore more articles on Asia Economy for in-depth financial news and analysis.