The Future of Lending: Why Income, Not Just Credit, Will Define Access to Capital

For decades, the three-digit credit score has reigned supreme as the arbiter of financial opportunity. But a growing movement is challenging this status quo, shifting the focus from past credit history to current income and earning potential. Platforms like Pennie are leading the charge, and their success signals a potentially seismic shift in the lending landscape. But is this a temporary trend, or a glimpse into the future of finance?

The Cracks in the Credit Score System

The traditional credit scoring model, while intended to assess risk, often penalizes those who need access to capital the most. Job loss, medical emergencies, divorce – life happens. These events can significantly damage a credit score, creating a vicious cycle where a low score limits access to loans needed for recovery. According to a 2023 report by the Consumer Financial Protection Bureau (CFPB), over 45 million Americans are considered “credit invisible” or have limited credit histories, disproportionately impacting minority communities and young adults.

This isn’t just a matter of fairness; it’s a matter of economic efficiency. Ignoring the earning potential of millions of capable borrowers means missed opportunities for economic growth. The rise of the gig economy and non-traditional employment further exacerbates the problem, as traditional credit models struggle to accurately assess income from multiple sources.

Income-Based Lending: A Growing Tide

Income-focused lending isn’t entirely new, but its adoption is accelerating. Fintech companies, unburdened by the legacy systems of traditional banks, are at the forefront. They leverage technology to verify income quickly and accurately, using bank statement analysis, payroll data, and even alternative data sources like utility bill payments.

Did you know? Bank statement analysis can provide a more comprehensive picture of a borrower’s financial health than a credit score alone, revealing consistent income deposits and responsible spending habits.

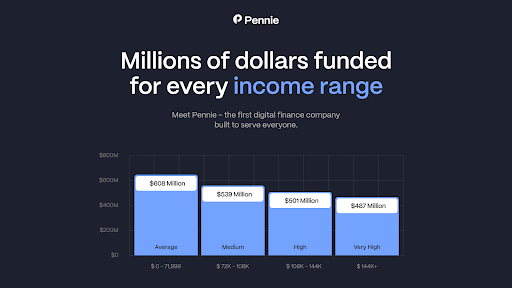

The numbers tell a compelling story. Pennie, for example, has facilitated over $350 million in loan offers in 2024 alone, funding over 32 million people. This demonstrates a clear demand for alternative lending solutions. Other companies, like Upstart, are also incorporating alternative data into their lending models, reporting lower loss rates compared to traditional credit-based lending.

Beyond Fintech: Traditional Banks Take Notice

The success of fintech disruptors isn’t going unnoticed by traditional financial institutions. Many are beginning to explore incorporating alternative data and income verification methods into their own lending processes. This isn’t about abandoning credit scores entirely; it’s about augmenting them with a more holistic view of the borrower.

However, challenges remain. Regulatory hurdles, data privacy concerns, and the need for robust fraud prevention measures are slowing down widespread adoption. The CFPB is actively researching and developing guidelines for the use of alternative data in lending, aiming to balance innovation with consumer protection.

The Role of AI and Machine Learning

Artificial intelligence (AI) and machine learning (ML) are poised to play a crucial role in the future of income-based lending. AI algorithms can analyze vast amounts of data to identify patterns and predict creditworthiness with greater accuracy than traditional methods. ML models can continuously learn and adapt, improving their predictive power over time.

Pro Tip: Look for lenders who are transparent about their use of AI and how it impacts lending decisions. Understanding the algorithm can help you understand your loan options.

This technology also enables more personalized loan offers, tailored to the individual borrower’s financial situation. Instead of a one-size-fits-all approach, lenders can offer customized rates and terms based on a comprehensive assessment of risk and potential.

Future Trends to Watch

- Expansion of Alternative Data Sources: Expect to see lenders incorporating more non-traditional data points, such as rental payment history, utility bill payments, and even social media activity (with appropriate privacy safeguards).

- Real-Time Income Verification: Technologies that allow for real-time income verification, such as direct integrations with payroll providers, will become increasingly common.

- Increased Regulatory Scrutiny: As income-based lending grows, regulators will likely increase their oversight to ensure fairness, transparency, and consumer protection.

- Embedded Finance: Lending will become increasingly integrated into everyday platforms and services, making it easier for borrowers to access capital when and where they need it.

FAQ: Income-Based Lending

Q: Will income-based lending hurt my credit score?

A: Not necessarily. Many platforms, like Pennie, use “soft-pull” credit checks that don’t impact your score.

Q: Is income-based lending more expensive?

A: Not always. Rates can vary depending on your profile and the lender, but income-focused lenders often offer competitive rates, especially for borrowers with limited credit history.

Q: What if my income is irregular?

A: Many income-based lenders can accommodate irregular income streams, such as those from gig work or freelance projects. You may need to provide additional documentation to verify your earnings.

Q: Is my data safe with these platforms?

A: Reputable platforms prioritize data security and privacy. Look for platforms with strong security measures and a clear privacy policy.

The future of lending is undoubtedly evolving. While the credit score won’t disappear overnight, its dominance is being challenged. By embracing income-focused approaches and leveraging the power of technology, lenders can unlock access to capital for millions of Americans and create a more inclusive and equitable financial system.

Want to learn more about your lending options? Explore Pennie’s platform to see if you qualify for a loan based on your income.