The Unwinding of Ultra-Low Mortgage Rates: What’s Next for Housing?

The era of historically low mortgage rates, fueled by Federal Reserve policy during and after the pandemic, is definitively coming to an end. Recent data reveals a steady decline in the share of mortgages below 3% and 4%, signaling a significant shift in the housing market landscape. But what does this mean for homeowners, potential buyers, and the broader economy?

The “Lock-In” Effect and its Consequences

Millions of homeowners secured incredibly low rates between 2020 and 2022. These rates, often below the prevailing inflation rate, represented a unique financial advantage. However, this advantage has created a “lock-in effect.” Homeowners are hesitant to sell, even if life circumstances change, because trading their 2.5% or 3% mortgage for a current rate of 6.5% or higher is financially unappealing.

This reluctance to sell is constricting housing supply, exacerbating affordability issues, and slowing down overall market activity. According to Redfin, new listings were down 21% year-over-year in January 2024, a direct consequence of this lock-in effect. The National Association of Realtors reports that existing-home sales remain below pre-pandemic levels.

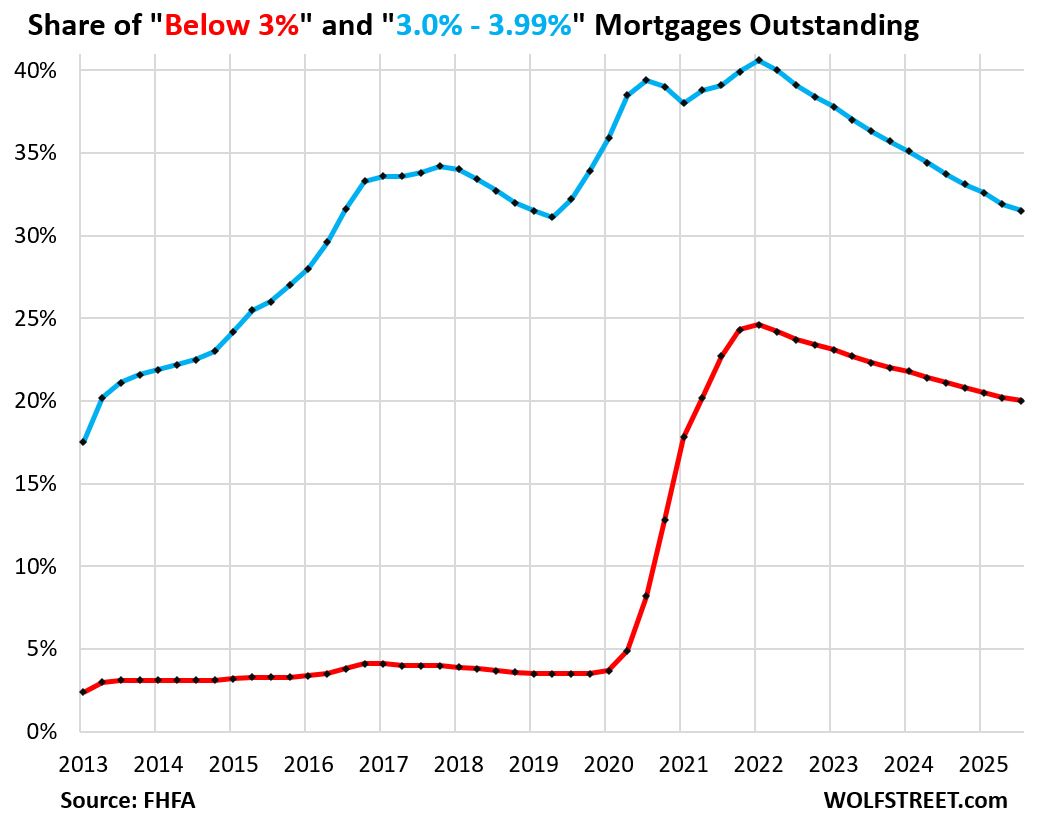

The Gradual Shift in Mortgage Rate Distribution

The share of mortgages under 3% has fallen to 20% as of Q3 2023, the lowest since early 2021. Simultaneously, the percentage of mortgages between 3% and 4% is also decreasing. Conversely, the proportion of mortgages at 6% or higher is steadily climbing, reaching levels not seen since 2015. This isn’t a sudden collapse, but a gradual unwinding – a slow bleed of ultra-low rates out of the system as homes are sold and refinanced.

Pro Tip: If you’re considering selling, carefully analyze the financial implications of your current mortgage rate versus the cost of buying a new home at prevailing rates. A financial advisor can help you navigate this complex decision.

The Impact on Adjustable-Rate Mortgages (ARMs)

While ARMs once represented a significant portion of the mortgage market, their share has remained relatively low since 2021, currently around 4%. The initial surge in rates in 2022 did cause “payment shock” for some ARM holders, but the worst of that impact appears to have passed. However, the risk remains for those with ARMs tied to indices that are likely to continue fluctuating with economic conditions.

What’s Driving the Change? The Fed’s Role and Inflation

The Federal Reserve’s aggressive interest rate hikes, implemented to combat inflation, are the primary driver of this shift. The Fed’s balance sheet reduction, reversing the massive asset purchases of the pandemic era, has also contributed to higher mortgage rates. While inflation has cooled from its peak, it remains above the Fed’s 2% target, suggesting that rates are unlikely to fall dramatically in the near future.

Did you know? During the height of the pandemic, “real” mortgage rates (adjusted for inflation) were negative, meaning borrowers were effectively being paid to borrow money.

Future Trends and Potential Scenarios

Several scenarios could unfold in the coming months and years:

- Scenario 1: Gradual Rate Decline. If inflation continues to moderate and the Fed begins to cut rates, we could see a gradual decline in mortgage rates, potentially easing the lock-in effect and boosting housing supply.

- Scenario 2: Rate Stabilization. Rates may stabilize at current levels, prolonging the lock-in effect and continuing to constrain housing inventory.

- Scenario 3: Further Rate Increases. If inflation proves more persistent than expected, the Fed may be forced to raise rates further, exacerbating the challenges in the housing market.

Regardless of the scenario, the housing market is likely to remain sensitive to economic data and Fed policy decisions. The pace at which the ultra-low rate mortgages are “unlocked” will be a key indicator of the market’s health.

The Ripple Effect on Related Industries

The slowdown in housing transactions is having a ripple effect on related industries, including mortgage lending, real estate brokerage, home improvement, and furniture sales. As reported by the Mortgage Bankers Association, mortgage origination volume has plummeted in recent quarters, leading to significant job losses in the mortgage industry. This contraction is a stark reminder of the interconnectedness of the housing market and the broader economy.

FAQ

- Q: Will mortgage rates go down in 2024? A: It’s uncertain. Rate movements depend heavily on inflation and the Federal Reserve’s actions. Most experts predict modest declines, but significant drops are unlikely.

- Q: What is the “lock-in effect”? A: It’s the phenomenon where homeowners are reluctant to sell because they have very low mortgage rates and don’t want to take on a higher rate on a new home.

- Q: Are ARMs a good option now? A: ARMs can be attractive if you plan to sell before the rate adjusts, but they carry the risk of higher payments if rates rise.

- Q: How does inflation affect mortgage rates? A: Higher inflation typically leads to higher mortgage rates, as the Federal Reserve raises interest rates to combat inflation.

The unwinding of the ultra-low mortgage rate era is a complex process with far-reaching implications. Understanding these dynamics is crucial for homeowners, potential buyers, and anyone invested in the housing market. Staying informed about economic trends and Fed policy will be essential for navigating this evolving landscape.

Explore more insights on housing market trends at WOLF STREET.