The Silver Tsunami Invests: How Baby Boomers Are Reshaping the Financial Landscape

For decades, financial planning centered around saving for retirement. Now, a novel phase is unfolding: retirement during a period of unprecedented longevity and economic strength for a specific generation. Baby Boomers – those born between 1958 and 1977 in Spain and 1946-1964 in the US – are not simply entering retirement; they’re redefining it. This demographic is increasingly financially secure, with over half owning their homes outright and a growing appetite for sophisticated investment products.

From Savings Accounts to Sophisticated Investments

The traditional image of retirees cautiously managing bank accounts is fading. Today’s Boomers are actively seeking out financial instruments beyond basic savings. Funds, life-insurance savings plans, and lifetime annuities are gaining popularity. Notably, there’s a growing willingness to embrace risk, a shift from previous generations.

This change is driven, in part, by increased life expectancy. Women retiring now can expect to live another 24 years, while men can anticipate 20 years of post-work life. This extended timeline allows for a longer investment horizon, even while drawing income.

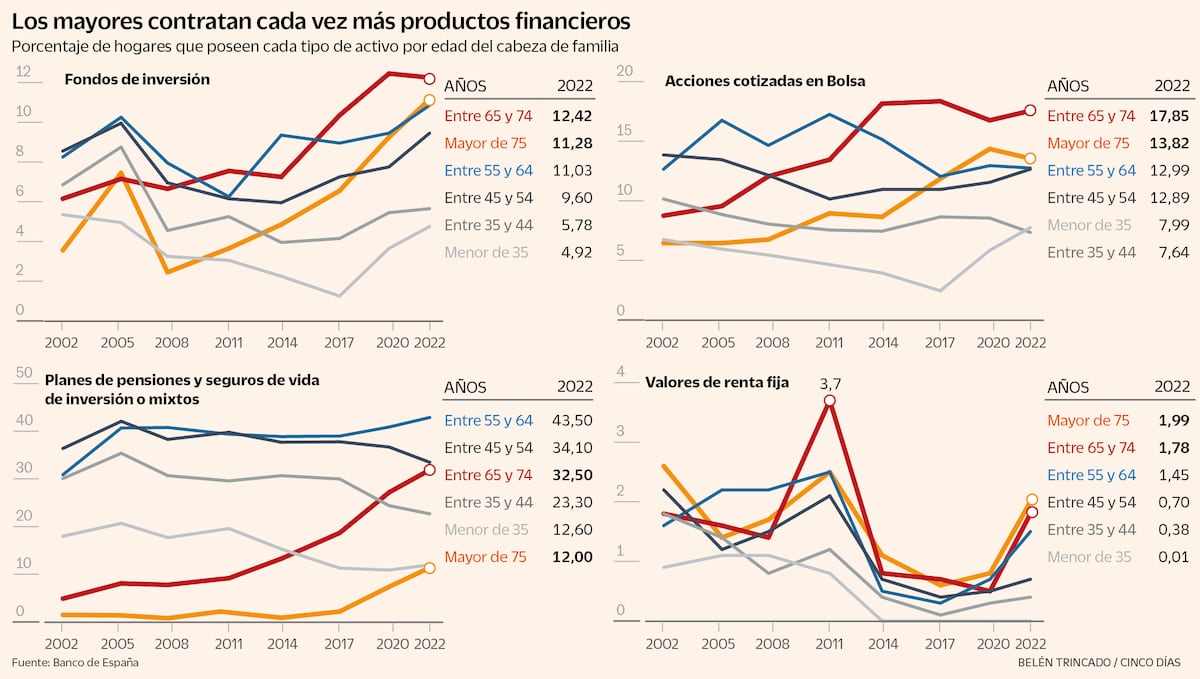

The Strain on Public Pensions and the Rise of Private Solutions

The longevity boom presents a challenge to public pension systems. In 2025, over 200 billion euros were allocated to pension payments, representing more than a third of total public expenditure. As more Boomers retire, the reliance on tax revenue to fund these pensions is increasing. This is prompting a shift towards greater individual responsibility for retirement income.

there’s a growing need for financial products and insurance to supplement public pensions. The proportion of individuals aged 65-74 with life-insurance savings or pension plans has risen from less than 4% two decades ago to over 32% today. Even those over 75 are increasingly investing, with over 11% holding investment funds – a significant increase from under 4% in 2011.

Rethinking Risk Tolerance in Retirement

Conventional wisdom once dictated a conservative investment approach as retirement neared – shifting heavily into bonds. Whereas, this strategy is being reevaluated. With potentially 20+ years of retirement ahead, a purely conservative portfolio may not generate sufficient returns to maintain lifestyle. Financial advisors are now suggesting that maintaining some exposure to equities, even in retirement, is reasonable.

The key is finding the right balance. Just as individuals have varying risk tolerances in hobbies – some enjoy mountaineering, others prefer quieter pursuits – investment strategies should be personalized. A “coffee with milk” analogy is being used: starting with a strong “coffee” (higher risk) when young and gradually adding “milk” (safer assets) as retirement approaches.

The Appeal of Lifetime Annuities

One product gaining significant traction is the lifetime annuity. These policies provide a guaranteed income stream for life, addressing the risk of outliving savings. Spain now holds 215 billion euros in policies combining life insurance and financial components – double the amount held in pension plans.

Lifetime annuities offer tax advantages, particularly when funded by the sale of a property. For example, a widow selling a house can defer taxes on capital gains up to 240,000 euros by investing the proceeds in a lifetime annuity. The income received from these annuities is taxed at lower rates for older individuals.

Estate Planning and Inheritance

Estate planning is as well becoming a priority. Investment funds offer tax benefits upon inheritance, as gains are not taxed. Pension plans, however, are treated as income and taxed accordingly. Lifetime annuities allow beneficiaries to be designated and can be structured to provide for both income and inheritance.

Financial institutions are responding to this demographic shift. CaixaBank, for instance, has launched a dedicated commercial offering for senior clients, “Generación +”, recognizing the growing economic power and unique needs of this cohort.

Frequently Asked Questions

Q: What is the typical age range for Baby Boomers?

A: In Spain, Baby Boomers are generally considered those born between 1958 and 1975. In the US, the range is 1946-1964.

Q: Are public pensions sustainable given increasing longevity?

A: The increasing burden on public budgets is a concern, leading to a greater emphasis on private retirement savings.

Q: What are lifetime annuities?

A: Lifetime annuities provide a guaranteed income stream for life, helping to mitigate the risk of outliving savings.

Q: How do investment funds compare to pension plans in terms of inheritance tax?

A: Investment funds generally offer more favorable inheritance tax treatment than pension plans.

Did you know? The longest retirement is expected for women, with a projected life expectancy of 25.5 years beyond age 65 by 2040.

Pro Tip: Don’t automatically reduce your investment risk as you approach retirement. A diversified portfolio with some exposure to equities can help maintain your lifestyle for a longer period.

What are your thoughts on the changing landscape of retirement planning? Share your comments below!