Global Markets on Edge: Geopolitical Tensions and Economic Signals

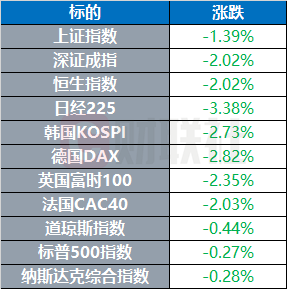

Global markets experienced a broad-based sell-off on Thursday, March 19, 2026, as escalating tensions in the Middle East combined with existing economic uncertainties. US stock indices closed lower, with the Dow Jones Industrial Average falling 0.44%, the Nasdaq Composite dropping 0.28%, and the S&P 500 declining 0.27%. European markets mirrored this trend, with the German DAX index leading the decline, falling 2.82%.

Middle East Conflict Fuels Market Volatility

The primary driver of market anxiety remains the escalating conflict in the Middle East. Reports indicate a potential Israeli strike on Iranian energy facilities, prompting a warning from the US President to avoid such action. Further complicating matters, Iranian officials claim their air defenses have successfully targeted a US F-35 fighter jet, though its fate remains unconfirmed. Israel’s Chief of Staff has stated that military operations against Iran are “not even halfway” complete, signaling a prolonged period of instability.

The US Department of Defense is seeking over $200 billion in funding for operations related to the conflict, underscoring the potential for a significant and sustained military commitment. This escalation is impacting investor sentiment, leading to a flight to safety and increased risk aversion.

Commodity Markets React to Uncertainty

Commodity markets are reflecting the heightened geopolitical risk. While international oil prices presented a mixed picture – WTI crude oil falling slightly to $96.14 per barrel and Brent crude rising to $108.65 – precious metals experienced significant declines. Spot gold fell 3.42% to $4653.01 per ounce, and COMEX gold futures dropped 4.86% to $4657.80 per ounce. Silver also saw substantial losses, with spot prices down 3.33% and COMEX futures falling 6.29%.

Economic Data Adds to Concerns

Adding to the market’s woes, US recent home sales in January fell to their lowest level since 2022, indicating a cooling housing market. Affordability issues continue to weigh on potential buyers, despite developer incentives and price reductions. The probability of the Federal Reserve maintaining interest rates at current levels in April stands at 92.8%, with a 7.2% chance of a 25 basis point increase.

Tech Sector Faces AI Concerns and Investor Scrutiny

Even the technology sector, a recent driver of market gains, is facing headwinds. Nvidia CEO Huang Ren-hoon has urged tech leaders to avoid fueling public fears about artificial intelligence, recognizing the importance of the technology but acknowledging potential risks. Meanwhile, outflows from US junk bond funds are potentially on track for their highest level in 11 months, reflecting growing credit concerns amid the broader market uncertainty.

Ukraine Peace Talks to Resume

Amidst the Middle East crisis, efforts to revive peace talks regarding Ukraine are underway. Ukrainian representatives are scheduled to meet with US officials on March 21st, marking the first bilateral meeting since the escalation of conflict in the Middle East. Ukraine’s President Zelenskyy expressed hope that these talks will lead to a meaningful resolution.

Looking Ahead: Potential Future Trends

The current market environment suggests several potential trends in the coming months:

Increased Geopolitical Risk Premium

Expect a sustained higher geopolitical risk premium in asset pricing. Investors will likely demand greater compensation for holding assets exposed to geopolitical instability, potentially leading to lower valuations and increased volatility.

Safe-Haven Demand

Demand for safe-haven assets, such as US Treasury bonds and the Japanese Yen, could increase further. This could set downward pressure on bond yields and potentially strengthen the Yen against other currencies.

Energy Price Volatility

Energy prices are likely to remain volatile, sensitive to any further escalation in the Middle East. Supply disruptions could lead to significant price spikes, while a de-escalation could result in price declines.

Slower Economic Growth

The combined impact of geopolitical tensions, higher energy prices, and tighter financial conditions could lead to slower global economic growth. This could weigh on corporate earnings and further dampen investor sentiment.

Focus on Defensive Sectors

Investors may shift towards defensive sectors, such as healthcare, consumer staples, and utilities, which are less sensitive to economic cycles and geopolitical risks.

FAQ

Q: What is the DAX index?

A: The DAX index is a German stock market index consisting of 40 major German companies.

Q: What is driving the decline in gold prices?

A: The decline in gold prices is likely due to a flight to safety towards the US dollar and reduced risk aversion as investors assess the situation.

Q: What is the outlook for US interest rates?

A: The market currently anticipates the Federal Reserve will likely hold interest rates steady in April.

Q: How will the conflict in the Middle East impact global supply chains?

A: The conflict could disrupt oil supplies and shipping routes, leading to higher transportation costs and potential supply chain bottlenecks.

Did you know? The DAX index is considered a key indicator of the German economy and European market health.

Pro Tip: Diversifying your portfolio across different asset classes and geographies can help mitigate risk during periods of market volatility.

Stay informed about global market developments and consider consulting with a financial advisor to make informed investment decisions. Explore more articles on our website or subscribe to our newsletter for regular updates.