Million-Dollar HDB Flats: Navigating the New Reality in Singapore

The Singaporean housing market is constantly evolving, and one of the hottest topics buzzing among residents is the increasing number of HDB flats selling for over a million dollars. While these transactions were once rare, they’re becoming increasingly common. Let’s dive into what this means for you and the future of Singapore’s housing landscape.

The Rise of Million-Dollar HDBs: A Trend in Motion

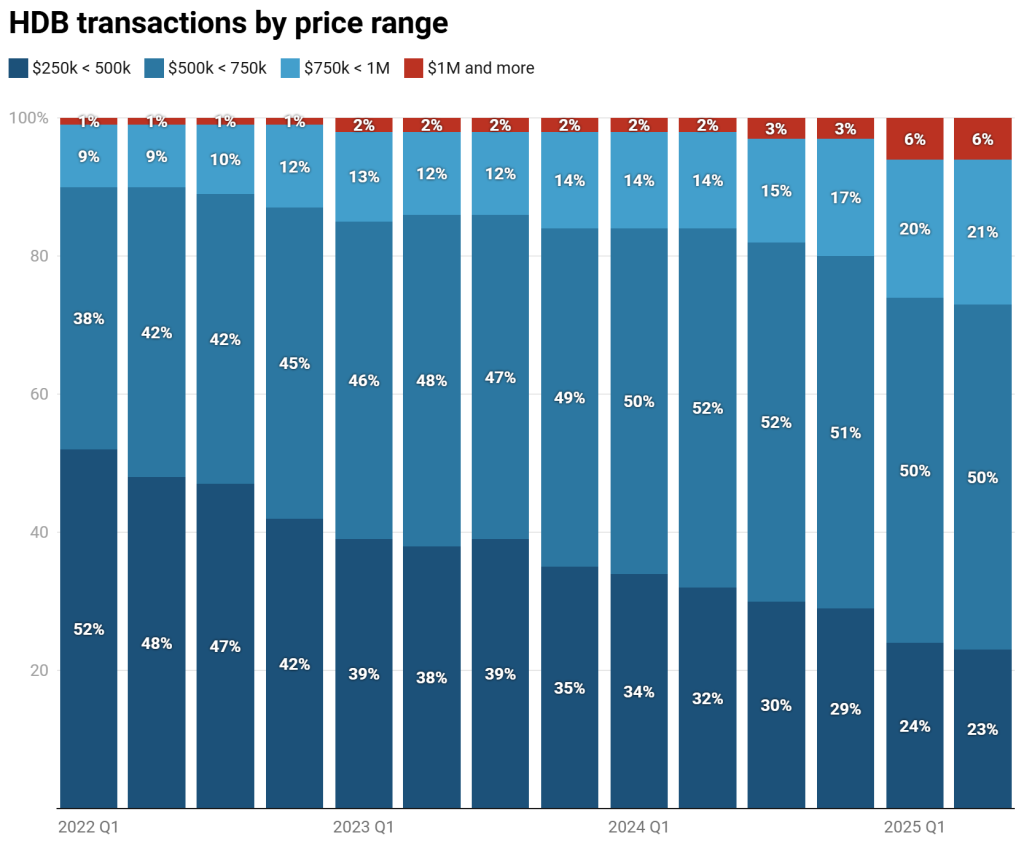

The article you provided highlights a significant shift. The proportion of million-dollar HDB transactions has jumped from under 1% to over 6% in a short timeframe. This surge is fueled by various factors, including rising inflation, a strong demand for spacious homes (partly stemming from work-from-home arrangements), and the overall desirability of mature estates.

The data speaks volumes. In 2024, over 1,000 HDB homes fetched prices above S$1 million. And the first half of 2025 already shows a robust number, suggesting the trend is accelerating. This isn’t just about a few high-end units; a significant portion of resale flats are now priced in the S$750,000 to S$1 million range, potentially pushing even more into the million-dollar category soon.

Did you know? The first million-dollar HDB flat sale occurred back in 2012. However, the frequency of these transactions has seen an unprecedented increase in recent years.

Understanding the Bigger Picture: Historical Context and Economic Realities

To put things in perspective, it’s helpful to remember that rising property prices are not new to Singapore. As incomes have increased over the decades, so too have housing costs. The key is to examine the relationship between income and housing prices.

In the late 1970s, when executive apartments were first introduced, they commanded prices that seem high for their time. Fast forward, and while prices have increased, so have salaries. Singapore’s HDB market remains one of the most affordable in the Asia-Pacific region, a testament to the government’s continued efforts to ensure housing remains accessible.

Pro tip: Compare the ratio of housing prices to annual household income. This provides a clearer picture of affordability than simply looking at the absolute price tag.

Inflation, Mortgages, and Your Financial Future

Inflation, often viewed negatively, can have a silver lining for homeowners with mortgages. As housing prices inflate, your asset’s value grows. Meanwhile, your mortgage payments remain relatively stable. This can be particularly beneficial for those nearing retirement, as a well-performing property can significantly boost their retirement funds.

For those considering buying, this trend reinforces the importance of strategic planning. Purchasing property is more than just securing a home; it’s an investment in your future. The potential for capital appreciation offers a safeguard against the rising costs of living, especially as you get older.

The Critical Role of Resale HDBs in Retirement Planning

Your home often forms the backbone of your retirement nest egg. As you consider downsizing or relocating, the value of your property becomes a critical financial resource. The appreciation in HDB values enables you to leverage your housing equity, providing funds for retirement or healthcare expenses.

This is especially important as consumer goods and services steadily become more expensive. If your home’s value keeps pace, you’ll be better positioned to maintain your lifestyle during retirement. The article argues that a steady increase in housing values is, in many ways, advantageous for long-term financial security.

Learn more: Explore our article on Retirement Planning in Singapore to delve deeper into this topic.

Finding the Sweet Spot: The Ideal Balance in the Housing Market

The perfect housing market doesn’t involve drastically low or high prices. Instead, it requires a balance that allows prices to grow in tandem with incomes and somewhat faster than overall consumer prices. This ensures that housing remains accessible while also providing a viable investment.

Ultimately, it’s not the absolute price of an HDB flat that matters. The crucial factors are how those prices evolve in relation to household incomes and inflation. Maintaining this balance is key for long-term stability and well-being.

FAQ: Addressing Your Burning Questions

- Are million-dollar HDBs a bubble? Not necessarily. While the prices are high, they are often supported by fundamental factors like rising incomes and limited supply.

- Should I buy an HDB now? It depends on your personal financial situation and long-term goals. However, rising prices can also mean increased equity over time.

- How can I afford an HDB? Explore government grants, consider your location preferences, and plan your finances carefully.

Ready to explore the market? Consult with a financial advisor to make an informed decision tailored to your circumstances.

Want to discuss the million-dollar HDB trend further? Share your thoughts in the comments below. Also, don’t forget to subscribe to our newsletter for more updates and insights on the Singapore property market!