The High Cost of Energy Dependence in Asia

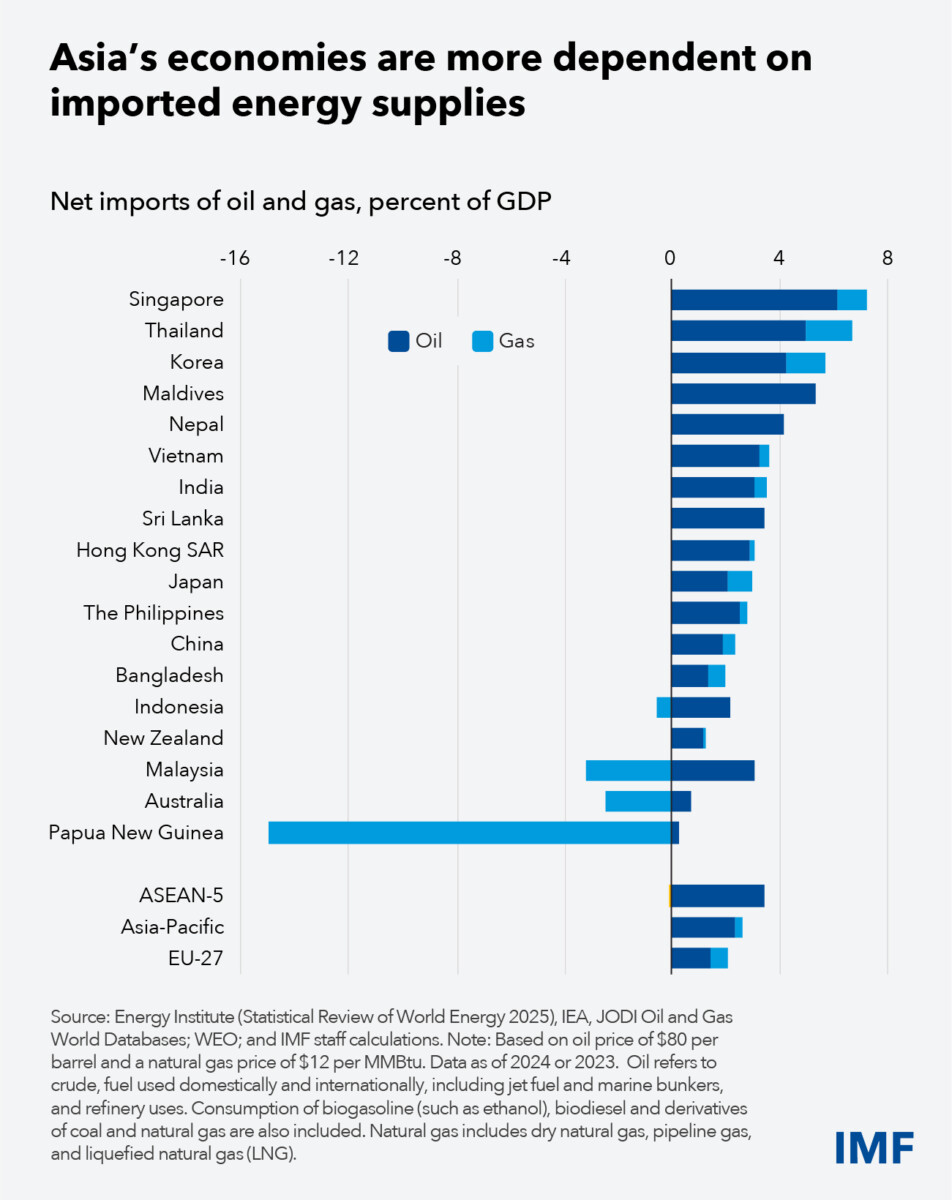

For many Asian economies, energy isn’t just a utility—it’s a primary economic vulnerability. Recent data from the IMF’s Asia Pacific Department highlights a stark reality: countries like Singapore, Thailand, and Korea maintain some of the highest levels of oil and natural gas import dependence relative to their GDP.

When global prices spike, these nations don’t just pay more at the pump. they experience a massive transfer of spending power toward oil-exporting nations. For instance, with Brent crude prices surging—peaking at $118 per barrel in April—the economic drain is significant. In Korea’s case, such price increases could constitute a transfer of 2.7 percentage points of GDP to exporters.

The “Net Zero” Illusion

A common misconception is that countries with a balanced oil trade or those that are net-zero importers are immune to energy shocks. In reality, because oil is priced on a global market, the cost of domestic oil rises alongside international benchmarks.

This creates a universal cost-push shock. Even the United States, despite its energy production capabilities, feels the ripple effects of global volatility. However, the impact is substantially larger in Asia due to the sheer intensity of energy consumption within its industrial bases.

Beyond the Price Tag: The Physical Supply Risk

While economists often focus on “paper prices” (futures), the real danger for East Asia lies in physical logistics. A significant portion of the region’s energy flows through the Strait of Hormuz, creating a strategic bottleneck.

The risk is not merely that oil becomes more expensive, but that it may actually disappear from the market. Most refineries in East Asia are specifically designed to process Gulf oil. If those supplies are disrupted, finding replacement crude isn’t as simple as paying a higher price; the physical infrastructure may not be compatible with alternative sources.

This distinction is critical. A price hike is an economic hurdle, but a physical shortage is a systemic failure that could lead to “demand destruction” and severe industrial shutdowns.

Divergent Paths: AI Tailwinds vs. Energy Headwinds

The global economic response to energy shocks is not uniform. We are seeing a widening gap between the resilience of the US economy and the vulnerability of Asia’s giants.

The US is currently benefiting from significant tailwinds, particularly massive investments in Artificial Intelligence (AI), which help offset the drag of higher energy costs. Conversely, the IMF’s forecasts show a slower growth trajectory for China and Japan, with projections dipping by 0.6 and 0.5 percentage points respectively compared to pre-war baselines.

The Adverse Scenario

In a worst-case “adverse” scenario, the IMF projects a 1% reduction in growth for Emerging and Developing Asia. This scenario assumes:

- Oil prices averaging $100 per barrel.

- Gas prices for Asia and Europe increasing by 160% relative to baseline.

- A “risk-off” episode increasing corporate premiums and sovereign spreads in emerging markets.

While oil exporters like Kazakhstan may notice short-term gains from higher prices, the IMF warns that commodity price volatility and trade disruptions do not stop at borders, leaving even the winners exposed to downside risks.

Frequently Asked Questions

How does oil price volatility affect GDP in Asia?

High import dependence means that as prices rise, a larger share of national income is transferred to oil-exporting countries, reducing domestic spending power and slowing overall GDP growth.

Why is the Strait of Hormuz so critical for East Asia?

It is a primary transit point for Gulf oil. Since many East Asian refineries are specifically designed for this type of crude, a blockage could lead to actual physical shortages regardless of the market price.

Can subsidies prevent energy-driven inflation?

They can mask inflation in the short term, but they impose heavy fiscal costs on governments and can be distortionary and difficult to remove once the crisis eases.

What are your thoughts on the shift toward energy diversification in Asia? Do you believe AI investments can truly offset energy-driven economic slowdowns? Let us know in the comments below or subscribe to our newsletter for more deep dives into global macroeconomics.

For further reading on regional outlooks, visit the IMF News Archive.