The Rising Tide of Household Debt: Navigating Current Trends and Future Implications

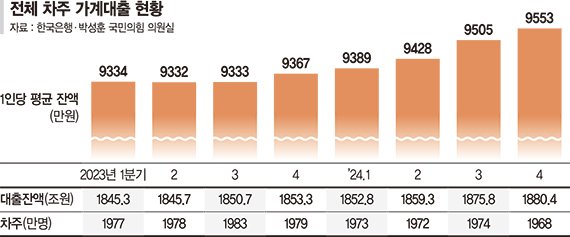

As of the last quarter of 2023, an alarming rise in household debt in Korea has been observed, with per capita household loan balances nearing a historic high of 9.53 billion KRW. This upward trend marks a 200 million KRW increase from the previous year, showcasing the growing financial burden on Korean households.

Understanding the Surge in Household Debt

A closer examination of recent statistics underscores the immediate need for intervention to curb the accumulation of household debt. Data from the National Assembly’s Planning and Finance Committee, provided by the Bank of Korea, highlights that the per capita loan balance rose from 9.367 billion KRW in 2023 Q4 to 9.53 billion KRW in 2024 Q4.

The trend has been escalating since Q1 2023, reaching 9.53 billion KRW in four consecutive quarters. Concurrently, while the total number of loan recipients saw a modest decline from 197.9 million to 196.8 million, the aggregate loan balance increased by 2.7 trillion KRW.

Demographic Insights: The Impact on Different Age Groups

Age-specific analysis reveals that 40-year-olds hold the highest average bank loan balance at 11.073 billion KRW, recording an all-time high, while individuals under 30 have also reached an unprecedented 7.436 billion KRW. Conversely, the 50+ age group experienced a reduction in their average loan balance by 10 million KRW.

Non-bank loans also demonstrate significant figures, with individuals under 30 holding an average of 3.969 billion KRW, elucidating the breadth of credit accessibility across different demographics.

Escalating Financial Vulnerability and Delinquency Rates

Financial vulnerability is increasingly evident with growth in late payment rates across banking sectors. The latest Financial Stability Report from the Bank of Korea indicates that by Q4 2023, the overall household loan delinquency rate rose to 0.93%, up from the previous year’s 0.86%.

Distinguishing between bank and non-bank sectors, delinquency in banks increased from 0.35% to 0.38%, while non-banks experienced a rise from 1.86% to 2.07%. A notable surge in the proportion of vulnerable debtors underscores the growing financial strain on households, with vulnerable borrowers comprising 6.9% of account holders in Q4 2023.

Tackling the Crisis: Proposed Measures and Policies

Highlighting the urgency, Assembly member Park Seong-hun emphasizes the need for comprehensive policy measures to alleviate the economic burden on vulnerable groups and prevent further escalation. Experts argue that failure to manage this debt spiral risks draining household consumption, thereby impeding economic growth.

Efforts are being called for in devising policies that can systematically reduce household debt while ensuring credit accessibility for critical needs.

FAQ: Key Concerns and Clarifications

What are the main causes of increased household debt?

The rise can be attributed to economic pressures, augmented borrowing due to rising costs of living, and possibly easy access to credit.

How can debt reduction be effectively managed?

Policy-driven solutions focusing on debt counseling, financial literacy programs, and regulatory frameworks to control lending practices are crucial.

Interactive Insights

Did you know? South Korea’s household debt-to-income ratio has consistently ranked among the highest in the Asia-Pacific region, spotlighting the need for urgent remedial measures.

Pro Tip: Households are encouraged to prioritize paying off high-interest debts first, alongside considering financial planning and management advice.

Call-to-Action: Join the Conversation

Do you think these measures will change the course of household debt trends? Share your thoughts and join the discussion by exploring more related articles or subscribing to our newsletter for updates on financial insights.

Worth a look