The Tightening Grip: Navigating the Future of the U.S. Fertilizer Industry

For decades, the backbone of American agriculture has relied on a steady, predictable supply of nutrients. But as we look toward the next decade, the landscape of the fertilizer industry is shifting from a broad, competitive field into a concentrated arena dominated by a handful of global titans.

Whether you are a large-scale producer or a family-run operation, understanding the structural changes in nitrogen, phosphate, and potash markets is no longer optional—it is a vital component of risk management.

A Market Defined by Giants: The Rise of Consolidation

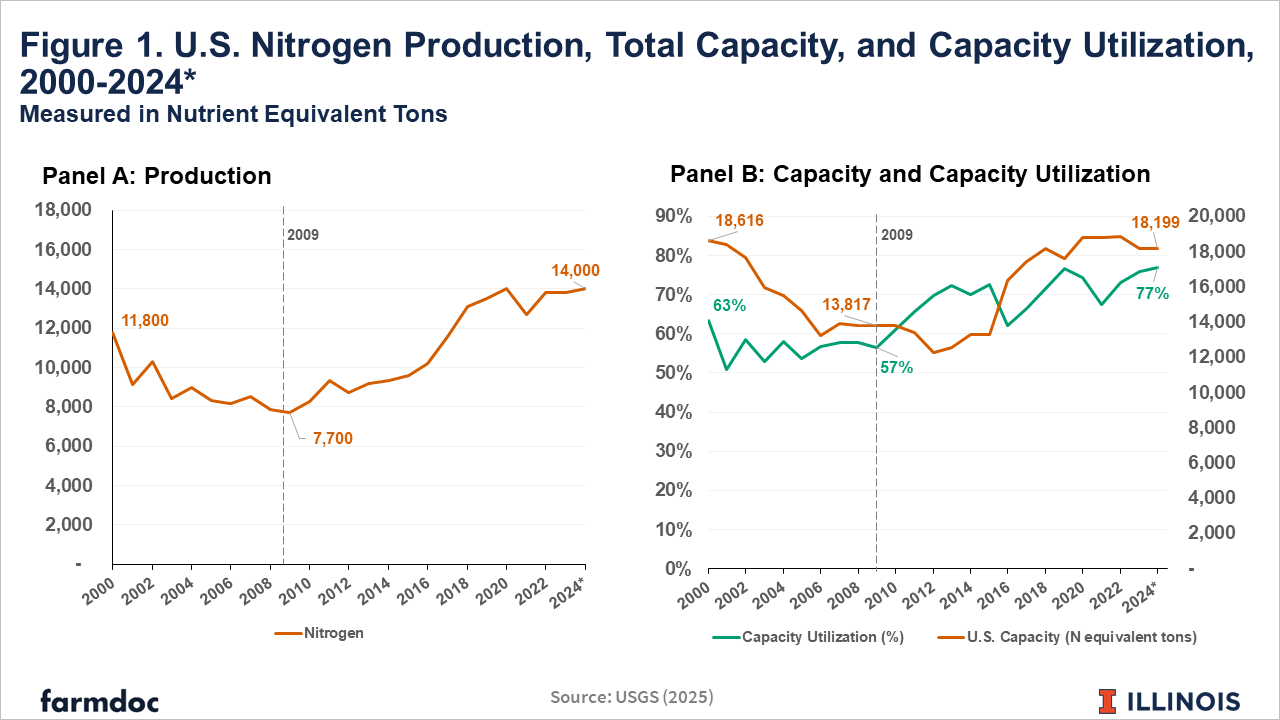

The most striking trend in the U.S. Fertilizer sector is the sheer scale of market concentration. In the nitrogen manufacturing space, the “huge players” aren’t just participants. they are the architects of the market. Currently, the top four companies control approximately 70% of U.S. Ammonia production capacity.

At the helm is CF Industries Inc., which commands a massive 39% of domestic production capacity. Following closely is Nutrien Ltd., holding a 16% share. This level of dominance isn’t just a statistic; it fundamentally alters how supply and demand interact.

The Herfindahl–Hirschman Index (HHI) is used by regulators to measure market concentration. The U.S. Nitrogen industry currently sits at an HHI of 0.201 (2,010 points), a level officially classified as “highly concentrated” under current Department of Justice guidelines.

This consolidation isn’t limited to nitrogen. The phosphate and potash markets show similar patterns. For instance, Nutrien and Mosaic together control over 89% of North American potash production capacity. When so much of the supply chain rests in a few hands, the traditional “rules” of competition often change.

The Regulatory Shadow: Will the DOJ Step In?

As the industry becomes more concentrated, the eyes of federal regulators are growing sharper. The 2023 update to the DOJ and FTC Merger Guidelines has lowered the threshold for what is considered a “highly concentrated” industry, making it easier for authorities to scrutinize large-scale transactions.

We are already seeing the ripple effects of this scrutiny. Recent investigations into whether major manufacturers coordinated to influence pricing suggest that the era of “business as usual” may be coming to an end. While an investigation does not equal a finding of wrongdoing, the mere presence of regulatory oversight can influence how these companies approach future mergers and acquisitions.

The Ripple Effect: From Manufacturing to Retail

It is a mistake to view this consolidation as something that only happens at the factory level. The influence of these giants extends deep into the retail sector. For example, Nutrien alone controls roughly 21% of the U.S. Retail industry.

This vertical integration—where a single company can produce the nutrient, manage the logistics, and sell it directly to the farmer—creates a powerful feedback loop. For producers, this means that the price you see at the coop is increasingly influenced by the same corporate strategies that govern global commodity markets.

Because individual farmers have limited ability to influence industry structure, focus on what you can control: forward pricing, precision application technology, and diversifying your supply sources to hedge against sudden price spikes.

Future Trends: What to Watch For

As we move forward, three key drivers will likely dictate the volatility and cost of agricultural inputs:

- Geopolitical Shifts: Conflicts in regions like Ukraine and tensions in the Middle East continue to threaten global supply chains, often forcing a renewed—and expensive—focus on domestic production capacity.

- Environmental Regulation: Increasing mandates to reduce nitrogen runoff and carbon footprints will add compliance costs. These costs are almost inevitably passed down the value chain to the end user.

- Transparency Mandates: There is growing political momentum for increased pricing transparency and potential USDA-led analyses of the industry to ensure fair competition.

While consolidation is often a natural byproduct of a mature industry, the speed and scale of current shifts are unprecedented. For the modern farmer, staying ahead of these trends means watching the regulators as closely as you watch the weather.

Frequently Asked Questions

Why is fertilizer consolidation a concern for farmers?

High concentration reduces competition. When a few companies control the majority of the market, they have greater “market power,” which can lead to higher prices and less flexibility for buyers.

What is the HHI in the context of agriculture?

The Herfindahl-Hirschman Index (HHI) is a mathematical measure used by the DOJ to determine how concentrated an industry is. A higher score indicates more concentration and less competition.

Can farmers do anything to combat high fertilizer prices?

While farmers cannot change industry structure, they can manage risk through strategic timing of purchases, adjusting application rates based on soil testing, and utilizing forward-pricing contracts.

Stay Ahead of the Market

The agricultural landscape changes fast. Don’t get caught off guard by shifting regulations or market consolidations.

Subscribe to our industry insights newsletter to receive expert analysis delivered directly to your inbox.

Related reading